Key Points

- Parent PLUS borrowers face challenges with both repayment and loan forgiveness due to the latest updates to the One Big Beautiful Bill.

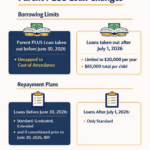

- Existing Parent PLUS loan borrowers must consolidate existing loans by July 1, 2026 to preserve access to income-driven repayment (IDR) plans.

- New Parent PLUS loans issued after July 1, 2026 will NOT qualify for income-driven repayment or Public Service Loan Forgiveness.

The massive federal budget bill moving through Congress is set to upend how parents pay for their children’s college education. The Senate passed its version of the bill on Tuesday, and it's expected to pass through the House by Thursday.

Sadly, the bill really impacts Parent PLUS borrowers - both current borrowers and future borrowers.

The reforms would bar Parent PLUS loans disbursed after July 1, 2026 from all income-driven repayment plans. This means that any parent who takes out a new PLUS loan for their child’s education after that date will be ineligible for any income driven repayment plans, including the new Repayment Assistance Plan (RAP).

Existing borrowers would also face challenges. Parent PLUS loans don't directly have access to income-driven repayment, but borrowers can consolidate their loans to access Income-Contingent Repayment (ICR). Borrowers must do this by June 30, 2026, or they will permanently lose access to this option.

Here's what Parent PLUS borrowers need to specifically know.

Would you like to save this?

No Income-Driven Repayment For New Parent PLUS Loans

While Parent PLUS loans don't directly have access to ICR, there has been a workaround for families. Borrowers could consolidate and enroll in the Income-Contingent Repayment (ICR) plan - the only IDR option available to them. Since ICR is PSLF-elgible, it also allowed parent to qualify for loan forgiveness.

Under the bill that just passed the Senate, that option disappears. Any Parent PLUS loan disbursed on or after July 1, 2026 will not be eligible for consolidation into ICR or access to any other income-driven plan. These loans must be repaid under the new Standard Repayment Plan.

While the bill introduces a new income-based option called the Repayment Assistance Plan (RAP), Parent PLUS borrowers are purposely excluded. RAP will only be available for other types of federal student loans. That means future parent borrowers will have no income driven repayment options or be able to qualify for loan forgiveness through PSLF.

Existing Borrowers Must Consolidate By June 2026 To Remain Eligible

Borrowers with existing Parent PLUS loans still have time to preserve access to income driven repayment and PSLF. To do so, they must:

- Consolidate their Parent PLUS loans before June 30, 2026, and

- Enroll in an income-driven repayment plan (ICR for single consolidation, any IDR plan for double consolidation)

Doing both steps ensures the borrower can enter the amended IBR plan, which continues under the new law for those with loans issued before the 2026 cutoff.

Failing to consolidate in time will forfeit this option permanently. Any new Parent PLUS loans taken out after July 1, 2026 will block borrowers and bar them from using income-based plans for any of their loans.

The latest bill has specific language that makes any loans taken after July 1, 2026 limited to the new standard repayment plan and the language says that the borrower has to pay all of their outstanding Parent PLUS Loans on that same plan (the Standard Plan).

If you have a Parent PLUS Loan, the only way to ensure you can continue income driven repayment or PSLF is by consolidating your loans before June 30, 2026.

PSLF Access Disappears For Future Borrowers

These repayment plan changes will also close off PSLF for parents who take out loans after the cutoff date. Since PSLF requires borrowers to make payments on an income-driven plan, the removal of IDR access effectively ends the program for future Parent PLUS borrowers.

Currently, parents who consolidate their PLUS loans into a Direct Consolidation Loan and enroll in ICR can make qualifying payments toward PSLF if they work in public service. After ten years of eligible payments, the remaining balance of the loan is forgiven.

That path disappears for new loans. The only remaining option (the standard repayment plan) pays off the full balance in ten years, leaving no remaining debt to forgive.

What Parents Should Do Now

With less than a year until the July 1, 2026 deadline, Parent PLUS borrowers may need to act soon. To preserve flexibility:

- Existing borrowers should stop taking out new Parent PLUS loans if they need ICR or PSLF. Any loan disbursed after July 1, 2026 disqualifies the borrower from all IDR plans.

- Consolidate existing Parent PLUS loans before the deadline.

- Enroll in ICR as soon as eligible. Waiting could increase the risk of losing access if rules or timelines change.

Once in ICR or amended IBR, borrowers can remain on the plan even after the new system takes effect. Those pursuing PSLF will retain access as long as they continue making qualifying payments.

Families relying on Parent PLUS loans to cover tuition gaps should consider other options now, including private loans. Once the bill take effect, new loans will come with stricter borrowing limits and far fewer protections.

Don't Miss These Other Stories:

Editor: Colin Graves

Robert Farrington is the founder of The College Investor and is widely recognized as one of the nation’s leading voices on student loan debt and saving for college. He holds an MBA from UC San Diego Rady School of Management and has spent over 15 years researching, writing, and advising on student loans, 529 plans, financial aid programs, and saving and investing for young professionals.

Robert has been featured in the The New York Times, The Wall Street Journal, The Washington Post, NBC News, and Forbes, where he has been a regular personal finance contributor for over a decade. His work combines both professional expertise and personal experience – he successfully navigated his own student loan repayment journey and has helped thousands of readers do the same.

He is committed to making the intersection of personal finance and education transparent and accessible. You can learn more about Robert on the About Page or on his personal site RobertFarrington.com.