This year, my employer started offering a Roth 401k for the first time. Although they’ve been around for a couple of years, only recently have more and more employers started offering them. I’ve been contributing to my traditional 401k since I was first able to, so I wasn’t sure about switching over to a Roth 401k.

This year, my employer started offering a Roth 401k for the first time. Although they’ve been around for a couple of years, only recently have more and more employers started offering them. I’ve been contributing to my traditional 401k since I was first able to, so I wasn’t sure about switching over to a Roth 401k.

Let’s break down the options and I’ll tell you what I decided.

How a Roth 401k Works vs. a Traditional 401k

If you want a full breakdown on a Roth 401k vs. Traditional 401k, read this.

A Roth 401k is like a Roth IRA. You put in after-tax money into the Roth 401k, and it grows over time tax free. When you contribute to a traditional 401k, you use pre-tax money, and it also grows tax free over time.

The big difference is at withdraw. With a Roth 401k, you don’t pay any taxes on the money (since you used after-tax money). With the traditional 401k, you have to pay income tax on it.

Another big difference happens when you get a company match. If your company matches your 401k contributions, those contributions are still pre-tax, and go into a traditional 401k. So, if you elect to have a Roth 401k, you basically have two accounts to keep track of: your pre-tax and your after tax account.

Should I Contribute to a Roth 401k?

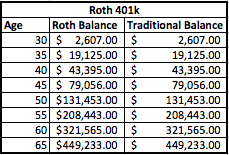

Let’s look at an example and break down the math. I’m going to use a hypothetical example of a person earning $50,000 per year and contributing 5% to his 401k. His company will also match 5% to the 401k. That means both he and his company contribute $2,500, making a total annual contribution of $5,000. Let’s say this starts when he is 30, and he plans to retire at 65. I also assume an 8% return.

Here’s how his accounts would look under both a traditional 401k plan and a Roth 401k plan:

As you can see, the balances are still the same after 35 years. The key difference is that the Roth 401k has the balances spread over two separate accounts – one pre-tax and the other after-tax.

However, it’s important to realize that you already paid taxes on the Roth balance. So, for every $1000 of pre-tax money you decide to put into a Traditional 401k, that equals $1250 [$1000 + 25% effective tax= $1250] of pre-tax money put in a Roth 401k in order to make the account balances equal.

Taxes Make The Difference

So which is better? It really all depends on your taxes. You see, with the traditional 401k, you only pay taxes on the money when your retire. With the Roth 401k, you have a hybrid version, where you don’t pay any taxes on the Roth 401k portion, but you will owe on the traditional 401k portion.

So, how will taxes impact you? Well, let’s look at it. We will use today’s tax brackets as an example, but remember that taxes are at historical lows, so they could rise in the future. Based on his current income, I would place this individual in either the 25% or 28% tax bracket. Let’s stick to the 25% bracket for now, and also estimate that he still wants to have about $50,000 per year in income. To get to that $50,000, we will withdraw $60,000 from each account and see what the tax situation looks like.

Traditional 401k

If he takes out $60,000 from the traditional 401k, he will face a Federal tax bill of roughly $8,060. Since all of the money is taxable when it’s withdrawn, he will have to plan for this when making withdraw decisions.

Roth 401k

On the flip side, if he has a Roth 401k, only 1/2 of the amount of money is taxable, just the portion in the traditional 401k account. So, if he withdraws $8,000, he is getting to withdraw $4,000 tax free and only has to pay tax on the remaining $4,000. This also means he can withdraw less than the original $60,000 to meet his goal. However, let’s stick to $60,000 to make a fair comparison (we’ll take $30,000 from the Roth portion and $30,000 from the traditional portion).

With a Roth 401k, his tax bill will drop to just $2,333.

That’s a single year tax savings of $5,727.

** However, remember that you already paid the tax on the Roth balance. Based on 35 years of Roth contributions, the tax paid on contributions over time equals $21,875 ($625 in taxes for 35 years). So, in reality, it takes about 5 years of withdrawals in retirement to break even. If your tax bracket is lower in retirement, the break even point is longer, and if your tax bracket is higher in retirement, your break even point is sooner.

My Thoughts on the Roth 401k

In my situation, I decided to go with the Roth 401k. I don’t see my tax bracket getting any lower in retirement, so it makes sense to pay taxes now and enjoy the benefits of more tax free withdrawals in retirement.

I think the example above really highlights the benefits of contributing to a Roth 4o1k. I had to sit down and do the math to see if it really made sense, and it does in my situation. However, it might not in every situation. Maybe someone can shed light on a situation when a Roth 401k doesn’t make sense?

Readers, what are your thoughts on a Roth 401k? Do you take advantage of it or are you sticking with your traditional 401k?

Editor: Clint Proctor Reviewed by: Chris Muller

Robert Farrington is the founder of The College Investor and is widely recognized as one of the nation’s leading voices on student loan debt and saving for college. He holds an MBA from UC San Diego Rady School of Management and has spent over 15 years researching, writing, and advising on student loans, 529 plans, financial aid programs, and saving and investing for young professionals.

Robert has been featured in the The New York Times, The Wall Street Journal, The Washington Post, NBC News, and Forbes, where he has been a regular personal finance contributor for over a decade. His work combines both professional expertise and personal experience – he successfully navigated his own student loan repayment journey and has helped thousands of readers do the same.

He is committed to making the intersection of personal finance and education transparent and accessible. You can learn more about Robert on the About Page or on his personal site RobertFarrington.com.