Utilities are the classic defensive investment. Generally slow-growing, but high-yielding and inexpensive relative to earnings, utilities are the traditional dividend value stock.

Utilities are the classic defensive investment. Generally slow-growing, but high-yielding and inexpensive relative to earnings, utilities are the traditional dividend value stock.

Now Wall Street seems to have turned on the utilities business. Should you listen?

What Utilities Really Are

An understanding of what utilities actually do really helps to explain why Wall Street might be putting them on the unlovable list. By and large, public-regulated utilities are merely financing operations for states and municipalities.

Regulated utilities raise capital to build a power plant, distribution networks, and establish their operations. Then, making their case to local regulators, utilities plainly state the cost of creating and delivering energy to a specific group of customers.

Most states establish a rate base, or the amount of money that the company can claim as an investment and maintenance expense each year to justify the cost of electricity per kilowatt of electricity or cubic foot of natural gas. Regulated utilities then charge customers a fee for use proportional to their energy consumption.

Regulated utilities essentially spend x dollars to build and maintain their facilities and infrastructure then seek approval to earn y% per year on their investment.

Unregulated utilities are an entirely different animal. Their markets are not guaranteed, there are no real monopolies, and competition can make for inconsistent cash flows when commodity prices change. One company’s coal plant may be more or less competitive to another company’s solar plant depending on coal prices, for example.

Why Utilities Rock

Utilities are awesome investments because of the following reasons.

They’re Recession-Proof

For the most part, the demand for electricity is consistent in all economic climates. You can be sure that the utility bill will be paid well before the mortgage or car payment — a life without electricity is no life at all.

They’re Easy to Understand

In the case of regulated utilities, a company builds its infrastructure then charges prices for energy and electricity based on the amount it invested into its fixed assets.

Cash Flows Regularly

While this industry can require large and infrequent investments, utilities do generate a significant amount of cash. This cash is rarely reinvested, and it is instead paid out to owners in the form of dividends.

Utilities always dominate lists of highest-yielding businesses, and they have impressive earnings payout ratios. (A payout ratio is the amount of earnings paid out as dividends to investors.) Utility companies also find it easy to finance major capital investments while paying consistent dividends.

My Dog Could Be a Utility CEO

You would have to try to fail to destroy a regulated utility company. As regulated utilities have guaranteed pricing, guaranteed customers, and a product that people simply cannot live without, the worst CEO you could imagine could steer a utility company successfully.

Utilities are (as far as I know) the only companies that posted profits continuously through the Great Depression, the largest economic downturn in U.S. history.

Why Wall Street Turned on Utilities

The very attributes that make utilities a great investment are the reasons why Wall Street isn’t too fond of utilities, as follows.

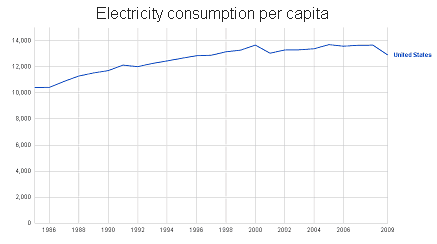

No Growth

Electricity and natural gas consumption is predictable — we know that growth will likely be proportional to population growth. Seeing as this country adds new people quite slowly — the population expands at about 0.7% to 1% per year — one should expect utilities to grow slower than your average S&P 500 component.

Valuations Are High

In a low-yield climate like we have now, investors snap up utilities like they’re going out of style. Currently, the utility industry trades at a 20% premium to the S&P 500 on a price-to-earnings basis.

Historically, it traded at a 20% discount to the S&P 500. Should valuations revert to the mean, stock prices will have to drop by 33%.

Bond-Like Attributes

Common stock in a utility company tends to trade a lot like a bond because the cash flows (dividends, in this case) are reliable, predictable, and unlikely to change significantly from year to year. Therefore, utility stocks rarely get the headline attention that highly volatile industries do.

Should You Buy Utility Stocks?

The answer is, as always, it depends.

If you’re happy to accept returns that will neither make you rich nor poor, utilities are a great place to put your money. With a current industry P/E of 16.9, you can expect to earn roughly 5.9% per year on your investment in the very long haul. You can also expect to have consistently increasing dividends over time.

However, you run into one serious (mostly short-term) risk: rising interest rates. If rates rise, high-yielding utilities are likely to fall out of favor, and share values will fall.

If you’re looking for outsized returns and can accept more volatility, look elsewhere. You’re not going to get rich quickly in the utilities business, although you will get fairly safe returns.

For these reasons, I would recommend to anyone to look at utilities as long-dated corporate bonds. Utilities tend to have similar convexity profiles in that utility stocks trade higher when interest rates go lower, and lower when interest rates go higher. The spread between utility dividend yields and the yield from a basket of long-dated investment-grade debt is fairly small.

It’s really a question of concentration: would you prefer to have big stock exposure to a single industry that is generally safe, or a diversified mix of bonds from companies in various industries that may be slightly riskier in the aggregate?

A value investor and blogger who enjoys discovering the hidden gems available on the public markets.

Editor: Clint Proctor Reviewed by: Chris Muller