Key Points

- The Department of Education administers federal student aid, but loan servicing and guarantee tasks involve many separate private contractors.

- Borrowers often encounter confusion and delays when navigating the higher education financing system.

- Proposals to shrink or eliminate the Department raise questions about who would handle key functions, but since many functions are outsourced, changes to the Department of Education may not cause significant interruption.

The Department of Education is in charge of the federal student loan system, along with many other tasks related to education, but much of the work is divided among various partners and contractors. The Department of Education is actually the smallest federal Department (with just over 2,000 after the layoffs a few weeks back). However, many of those employees actually oversee and/or partner with a large system of contractors, lenders, state agencies, and more.

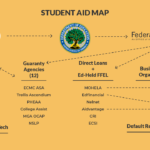

When it comes to higher education student aid, there's a complex web of partners that serve various roles.

For example, the Federal Family Education Loan (FFEL) Program once relied on over a hundred private lenders—Navient, Nelnet, ECMC, PHEAA, and others—to fund student loans. However, legislative changes phased out FFEL lending, and now government issues loans under the Direct Loan Program, although older FFEL accounts still exist.

Since 2010, all federal student loans have been issued directly by the Department of Education (hence "Direct" loan).

Guaranty agencies serve as insurers for those older FFEL loans. There are still 12 of these entities, including ECMC, ASA, Trellis, Ascendium, and PHEAA. They step in when defaults occur, reimbursing lenders for losses and working to recover overdue balances.

Meanwhile, the Department of Education continues to oversee Direct Loans and federal-held FFEL accounts through servicers like MOHELA, EdFinancial, Nelnet, and Aidvantage. These companies manage billing, payments, and account updates, often handling tasks such as enrollment in repayment programs. If a borrower defaults, the account can shift to the Default Resolution Group (DRG), operated by Maximus under contract.

Would you like to save this?

Most Functions Of The Department Are Handled By Contractors

When it comes to federal student aid (student loan specifically), most functions are outsourced.

According to Betsy Mayotte, President of The Institute of Student Loan Advisors, "Contractors handle almost all of [the] things like PSLF, processing consolidations, disability discharge, TEACH grant management, and of course the day to day servicing of the loans (such as accepting and posting payments, maintaining loan records, answering borrower emails and calls about their loans, processing deferments and payment plans)."

The first level of contractors are the well known student loan servicers. For Direct Loans, these include MOHELA, Edfinancial, Nelnet, Aidvantage, CRI, and ECSI. For FFEL loans, there are over 100 lenders, but many use loan servicers like Sloan (or even some of the main ones like MOHELA).

The next link in the chain is the set of Business Processing Organizations (BPOs). Entities such as MOHELA (in a separate role from their loan servicing department), FH Cann, EdFinancial, and Maximus handle phone lines, technical infrastructure, and other operational duties once managed by full-time federal ED employees.

So even when, on the outside, it appears that the Department of Education is managing programs like Public Service Loan Forgiveness directly, inside the organization, a BPO is actually handling most of the workload. Only when actual forgiveness is set to be granted, does an actual ED employee validate and approve.

Officials argue that outsourcing can improve efficiency by moving specialized tasks—like high-volume call centers—to private firms. Critics contend that this practice fragments the student loan system.

Each company may have its own procedures, creating a patchwork of policies. When borrowers move from one status to another, or when a servicer contract changes, records can get shuffled between separate databases. It's important to remember, while there is one master data file of student loan borrowers, the rest of the system is fragmented:

We saw this last week, when MOHELA was the first student loan servicer to announce the FSA-directed extensions of IBR recertification, meanwhile it took Aidvantage and Nelnet several days to get the information disseminated to their call center reps to provide the updated information to borrowers.

An Office of Inspector General report highlighted gaps in contractor management, pointing out that private operators sometimes lack clear directives on borrower communications and complaint handling. For instance, some BPOs faced criticism for inconsistent recordkeeping, leading to confusion about billing notices or deadlines. The OIG also noted that the Department’s reduced staffing has hampered efforts to monitor these contractors closely. Fewer employees are available to conduct routine audits or verify whether the BPOs are following federal guidelines.

So What Does The Department Handle Directly?

While many processes are handled by contractors, the Department of Education still has many functions they have to handle directly - some required by law. For example, final approval of loan forgiveness (specifically for PSLF) is mandated to be done by the Department of Education.

There are many functions written into the laws created by Congress that are required to be executed by a member of the Department of Education, or directly overseen if contracted out. While our focus is on higher education, this extends across the Department of Education.

Some other key things that are handled by employees of the Department of Education:

Functions Required By law

There are many functions that are required by law (written by Congress) that members of the Department of Education has to do.

Some examples that are in the existing statutes (there are many that impact higher education):

- Final PSLF loan forgiveness approval (this also includes things like buy back requests)

- Any discharge or cancellation approvals

- Consolidation approvals

- Required functions of the Individuals with Disabilities Education Act

- Oversight of Federal Pell Grant distribution

Oversight Of Contractors

Going back to that map above, there are a lot of contractors that the government pays millions of dollars to. There are employees who's job is to both negotiate these contracts, and then follow up on the execution of them. They also need to monitor performance (daily), to ensure that calls are processed, information is communicated, records are handled, and payments are made.

Policy

Congress passes laws, but it requires people to translate the laws into actual regulations and actions that can be taken. This requires lawyers and other experts who can put this together. Then, the policy needs to be translated to both the contractors and the general public.

Some aspects of policy might require other procedures, like negotiated rulemaking - another process created by Congress.

Communication

Once you have a policy created, you need to communicate this policy both internally and externally. This will require a team to both navigate contractor communications and training, and consumer communication and education. There are 43 million student loan borrowers, and they need to be informed.

And we know this can't be outsourced to AI, because AI gets financial information wrong an shocking amount of the time.

Statistics

There is a congressional mandate to collect, analyze, and report full and complete statistics on the condition of education in the United States. This was handled by an internal department called the National Center for Education Statistics. This department has existed in some way since the 1880s, and the data collected is required to be done so by law.

Consumer Complaints

If there are issues or concerns with the contractors, there needs to be an avenue for consumers to get resolution. The Department of Education needs to handle complaints and investigate them. In 2024, Federal Student Aid fielded over 130,000 complaints. That's 356 complaints per day, on average. Each of these complaints will take time to pull records, assess information, validate that the servicer did (or did not) do things correctly, and send a response.

In the case where things were not handled correctly, follow up actions on the loan servicers need to take place. This might go back to oversight or communication teams to education, or even fine loan servicers. That what happened with MOHELA in 2023.

Investigations

Taxpayers demand to know that there money isn't being wasted. So you also want to have teams that validate that money is being spent correctly. The Department of Education validates multiple angles: schools that receive aid (they have to be eligible and not hurting borrowers or taxpayers), individuals who could take out loans fraudulently, and all the contractors that could be wasting dollars.

This is a function that needs to happen - and it can prevent fraud and waste.

According to Mayotte, "Many if the employees that handled those functions were part of the RIF two weeks ago. Which to me, is ironic, as the point was to get rid of fraud and abuse – to me getting rid of these employees will do the opposite and make it easier for fraud to go unseen."

How Does The Department of Education Compare To Other Lenders?

President Trump remarked that "The Department of Education currently manages a student loan debt portfolio of more than $1.6 trillion. This means the Federal student aid program is roughly the size of one of the Nation’s largest banks, Wells Fargo. But although Wells Fargo has more than 200,000 employees, the Department of Education has fewer than 1,500 in its Office of Federal Student Aid. The Department of Education is not a bank, and it must return bank functions to an entity equipped to serve America’s students."

So, given the Department of Education (or whichever Department might oversee this in the future) manages $1.6 trillion - and is continuing to lend upwards of $100 billion in new student loans per year, is Federal Student Aid too big?

Well, Fannie Mae and Freddie Mac are home loan lenders, and they each manage about $3 to $4 trillion in loans. And they each do it with about 8,000 employees.

To contrast that, Ally, the nations largest auto lender, manages $86 billion in auto loans (and $136 billion in total loans). They have 10,000 employees.

Borrower Frustrations

Anyone holding a federal student loan can attest that it can be daunting to figure out who manages which piece of the puzzle. A single account might go from a private lender to a guaranty agency, then to a federal servicer, and potentially to a separate contractor if it goes into default. During these transitions, borrowers can lose track of overdue notices or information about repayment programs.

Even for Direct loans, we've seen a lot of loan servicer changes in the last few years, with Fedloan, GSMR, and Navient all deciding to stop servicing federal student loans.

Some individuals face long phone calls and repeated document submissions, only to discover their account has been reassigned. Each handoff between companies increases the odds that mistakes will happen or questions will go unanswered. Federal staff cutbacks add to that uncertainty, as fewer government employees are on hand to handle disputes or push for corrections.

It’s common to hear stories of borrowers being transferred multiple times in a single call, each representative pointing to a different office. Payment plan applications may sit in limbo if the servicer and the agency overseeing the account lack alignment. Borrowers report confusion over interest calculations, late fees, and which entity handles defaulted debt.

This is a problem that's grown dramatically as the number of loans has grown as well. Going back to 2010, the office of Federal Student Aid fielded over 30,000 complaints. For contrast, the loan portfolio in 2010 was roughly $450 billion, with $390 billion being FFEL loans.

While it may seem like going from 30,000 to 130,000 complaints in 15 years is a big jump, the loan portfolio has also grown to 1.7 trillion (from the $450 billion), and the number of loan repayment options and forgiveness programs have also increased. PSLF wasn't even signed into law until 2007, which meant the very first eligible people couldn't even apply for forgiveness until 2017. Fast forward to today, there are approximately 100,000 people achieving forgiveness under PSLF each year - each application which requires a manual review.

Department of Education Cuts And Layoffs

President Donald Trump has called for drastic measures, such as eliminating the Department of Education. While fully dismantling the agency would require an act of Congress, staff levels have already been reduced by roughly 50%. Those who remain are stretched across policy work, oversight, and direct borrower assistance.

With fewer federal employees, more responsibility could shift to contractors, lenders, and guaranty agencies. In fact, there has been talk of more privatization of student loans as well.

Observers warn that deeper cuts may undermine the agency’s capacity to supervise programs like Public Service Loan Forgiveness or keep track of how private contractors treat borrowers. Persistent oversight is often seen as a balancing measure when large corporations handle public programs.

If the Department’s workforce continues to dwindle, the possibility of miscommunication and errors may rise. Different contractors could interpret new regulations in conflicting ways. Call center wait times might grow. Borrowers seeking to disputes or request discharge for disabilities could find the process even more time-consuming.

Looking Ahead

Trump’s efforts to reduce the federal role in education have brought renewed focus on how the Department of Education—and the network of external partners—truly functions. Some analysts believe states or private organizations might take a greater role if the Department shrinks. Others warn that comprehensive oversight would be harder to maintain without a central body ensuring consistent application of rules.

"Borrowers are confused and anxious with all the recent announcements and executive orders. And as the ED related EO’s may not even be legal, it remains unclear the effects these will have in the long run. We do know that as most of the functions are done by vendors the general day to day shouldn’t change, and because the terms and conditions of the loans are set in federal law and regulations, access to benefits shouldn’t change either," says Mayotte.

For now, the attached map shows a system already spread among lenders, guaranty agencies, federal servicers, and third-party operators. The Department of Education has to deal with broad policy set by Congress, but leans on these contractors for day to day tasks. Borrowers caught in the middle may feel overwhelmed by the red tape, especially when accountability gets murky.

If further layoffs occur, many expect that outside contractors would absorb more duties. Whether that path leads to improved management or more confusion is uncertain. As political debate intensifies, the main concern for those owing student loans remains the same: staying afloat in a system where responsibility is sliced into many parts.

Related: Who's To Blame For The Student Loan Crisis

Those who are well-informed about their loans and keep thorough records may have an easier time, yet even the most organized borrowers can be stymied by a phone system or website glitch.

With every policy shift, question of department downsizing, or contractor shakeup, the student loan process grows more challenging to follow. Whether the Department of Education stands firm or downsizes further, the frustration remains: it takes effort and patience to find your way through a structure in which no single entity holds all the answers.

Don't Miss These Other Stories:

Editor: Colin Graves Reviewed by: Mark Kantrowitz

Robert Farrington is the founder of The College Investor and is widely recognized as one of the nation’s leading voices on student loan debt and saving for college. He holds an MBA from UC San Diego Rady School of Management and has spent over 15 years researching, writing, and advising on student loans, 529 plans, financial aid programs, and saving and investing for young professionals.

Robert has been featured in the The New York Times, The Wall Street Journal, The Washington Post, NBC News, and Forbes, where he has been a regular personal finance contributor for over a decade. His work combines both professional expertise and personal experience – he successfully navigated his own student loan repayment journey and has helped thousands of readers do the same.

He is committed to making the intersection of personal finance and education transparent and accessible. You can learn more about Robert on the About Page or on his personal site RobertFarrington.com.