Key Points

- The proposed “Student Success and Taxpayer Savings Plan” would repeal most existing income-driven repayment plans, replacing them with a single 30-year AGI-based repayment option.

- Current borrowers in the SAVE, PAYE, and newer IBR plans would lose access to those plans and could face significantly higher monthly payments or extended repayment terms.

- The proposed Repayment Assistance Plan (RAP) could offer manageable monthly payments for borrowers, but with longer repayment periods.

The Republican-backed student loan overhaul, advancing through the House, would upend nearly every repayment option available to borrowers. Gone would be the current mix of plans that let borrowers choose among varying monthly payments, timelines, and forgiveness options.

In their place, a new two-plan structure: a fixed standard plan based on loan amount, and a single income-based plan called the Repayment Assistance Plan, or RAP.

Under current law, borrowers can choose from multiple repayment plans, including income based repayment (IBR), Pay As You Earn (PAYE), Income-Contingent Repayment (ICR), and standard plans such as the Standard 10-Year, Extended, and Graduated Plans.

If the GOP proposal becomes law, plans like PAYE and the newer version of IBR would be repealed. Borrowers could instead choose RAP or old IBR, which mean borrowers could face higher payments.

Would you like to save this?

Shrinking Set of Choices

Under the bill’s language, current borrowers would not be totally grandfathered into their existing income-driven repayment (IDR) plans. What this means is that, for borrowers with loans originated before June 30, 2026, the only income-driven repayment plan available would be the old IBR plan (pre-2014 IBR). For many, this would lead to a noticeable jump in monthly payments.

Note: SAVE is also gone, but that is to be expected based on the current lawsuits.

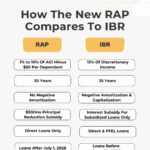

The pre-2014 IBR plan uses 15% of discretionary income, compared to 5% for SAVE and 10% for PAYE or new IBR. The shift would raise payments by 50% or more for some borrowers. For low-income households, those increases could strain already tight budgets.

The only other option, RAP, offers payment amounts based on income but comes with a 30-year timeline and no option to switch to another plan later.

Longer Timelines Also Can Mean More Interest

The new RAP plan, while income-based, comes with trade-offs that are drawing criticism. Under RAP, loan forgiveness would only come after 360 monthly payments, or a full 30 years. For comparison, current borrowers with new IBR is 20 years, and old IBR is 25 years.

RAP’s formula would keep monthly payments similar to PAYE and new IBR for many middle-income borrowers, but total repayment costs would likely be higher. Given the switch from discretionary income to AGI, while similar, could impact some families differently.

The longer term means more interest, and while unpaid principal can be deferred, interest will still be applied before reducing the principal.

Borrowers would also be locked into RAP after opting in, without the ability to switch to another income-based plan if their financial situation changes. This inflexibility has raised concerns about long-term affordability and borrower protection.

What Can Borrowers Do Now

The plan would simplify federal loan repayment plans, but at a cost. By removing PAYE, ICR, and newer IBR, borrowers lose plans with shorter timelines and stronger forgiveness protections. And while RAP offers a consistent framework, it leans more heavily on long-term repayment than debt cancellation.

It's important to note that the RAP and all of these changes are currently just a proposal. Borrowers don't nee to take any action now, except stay informed about what's happening, and contact their legislators if they want to voice their concerns.

When real changes happen, borrowers need to asses the options and understand what repayment plans may be available to them.

Other Questions

Which existing IDR plans would be eliminated under RAP?

Currently, the law proposes eliminating ICR, PAYE, and new-IBR, and leaving only the Old IBR option. It also removes any hardship requirements, meaning that all borrowers with loans before 2025 could opt for the IBR option.

How does RAP’s AGI-based formula differ from discretionary income?

The RAP is based on adjusted gross income, which is pulled from your tax return. Discretionary income is calculated on a formula based on 150% of your state's poverty line based on your family size. Here is our discretionary income calculator.

Should borrowers accelerate payments pre-2026?

My recommendation is for borrowers to continue to wait it out before making any changes. First, this proposal is still just a proposal. We don't know what the final version will look like (or if it will happen at all). Second, once we know it's official, you still want to decide which plan is best for you. Making extra payments on an income-driven repayment plan usually doesn't make sense.

Don't Miss These Other Stories:

Editor: Colin Graves

Robert Farrington is the founder of The College Investor and is widely recognized as one of the nation’s leading voices on student loan debt and saving for college. He holds an MBA from UC San Diego Rady School of Management and has spent over 15 years researching, writing, and advising on student loans, 529 plans, financial aid programs, and saving and investing for young professionals.

Robert has been featured in the The New York Times, The Wall Street Journal, The Washington Post, NBC News, and Forbes, where he has been a regular personal finance contributor for over a decade. His work combines both professional expertise and personal experience – he successfully navigated his own student loan repayment journey and has helped thousands of readers do the same.

He is committed to making the intersection of personal finance and education transparent and accessible. You can learn more about Robert on the About Page or on his personal site RobertFarrington.com.