Key Points

- 529 savings plans now cover a wider set of expenses for K-12 education, including books, online materials, and testing fees.

- Standardized test fees are explicitly covered, but test prep materials and courses remain a gray area.

- These new rules apply immediately to distributions made after the bill's enactment date (July 4, 2025), but the higher limit of $20,000 takes effect in 2026.

Parents using 529 savings plans to fund their children’s education have more options after Congress expanded the definition of "qualified expenses" to include a broader range of K-12 costs. The provisions, enacted as part of the recent One Big Beautiful Bill, took effect immediately and have raised questions about how families can now use these funds.

Families can begin using their 529 plans for these new qualified expenses immediately. Any distribution made after the date the law was enacted qualifies, which was July 4, 2025. That means parents can reimburse themselves for recent standardized test fees or classroom materials like back to school shopping.

However, the new higher limit of $20,000 doesn't take effect until 2026 - only the expanded expenses are eligible in 2025.

However, families should still keep documentation for all purchases in case of questions during tax time. The IRS requires clear records of qualified withdrawals, and this expanded list may increase scrutiny.

Furthermore, it's important to note that not every state will conform to the expanded rules. Some states, like California, are notorious for not conforming with federal 529 plan rules. Before you start spending your 529 plan funds, make sure you know your state's rules!

Editor's Note: Clarified the dates of both the expanded expenses and higher limits.

Would you like to save this?

What Changed For 529 Plan Rules?

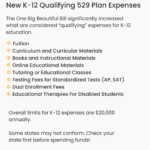

Prior to the update, 529 plans could be used for up to $10,000 per year in K-12 tuition, along with various higher education expenses like tuition, fees, books, room and board, and computers. Now, families may also use funds to cover:

- Curriculum and curricular materials

- Books and other instructional materials

- Online educational materials

- Tutoring or educational classes outside the home

- Testing fees for standardized tests and college entrance exams

- Dual enrollment fees for high school students taking college courses

- Certain educational therapies for students with disabilities

This change gives parents more control over how they manage education costs across all levels of schooling, not just college.

What's Covered For Standardized Testing?

One of the most immediate benefits for many families is the inclusion of testing fees. These include fees for:

- Nationally standardized norm-referenced achievement tests

- Advanced Placement (AP) exams

- College admission exams like the SAT and ACT

It's important to note that test prep is more of a gray area.

Is Test Prep Covered?

This question has drawn particular attention from test prep providers. Some argue that the new language could be interpreted to include preparation courses under sections referring to "online educational materials" or "tutoring or educational classes outside the home", especially for online test prep classes or even test prep books.

But there are limits. Under the new law, educational classes must be provided by someone with appropriate credentials:

- A teaching certificate

- A college degree

- Subject matter expertise in the relevant area

Test prep services often focus on exam strategies rather than traditional subject instruction. Unless the instructor holds relevant credentials and is teaching core academic content, it’s unlikely that generic SAT or ACT prep would qualify.

Also worth noting: the law lists testing fees as a separate, clearly defined category. According to college savings expert Mark Kantrowitz, "had lawmakers intended to include prep costs, it likely would have been mentioned alongside test fees. The separation suggests test prep is not included."

Duel Enrollment And Special Education

Parents of high school students enrolled in college courses can now use 529 funds to pay for those dual enrollment fees. This aligns with broader efforts to reduce college costs by supporting students who earn credits early.

For students with disabilities, the law also expands qualified expenses to include therapies. Covered services may include occupational therapy, physical therapy, and other education-related support services. These additions provide much-needed flexibility for families managing special education needs.

The law also permanently allows rollovers from regular 529 plans to ABLE accounts to support those with disabilities.

What This Means For Parents And Students

The expanded use of 529 plans gives families more ways to manage education expenses beyond just college costs. With curriculum and testing fees now included, families can make better use of their tax-advantaged savings.

Still, families hoping to cover test prep should approach the new rules with caution. Unless a provider meets the credentialing standards outlined in the law, prep classes likely remain out-of-pocket costs.

Parents should review their state’s 529 rules as well. While most states follow federal law on qualified expenses, about one-third of states set their own rules on what counts and what doesn't.

As education costs continue to grow at every level, these changes may offer some relief, but they don’t erase the need for careful planning.

Don't Miss These Other Stories:

Editor: Colin Graves

Robert Farrington is the founder of The College Investor and is widely recognized as one of the nation’s leading voices on student loan debt and saving for college. He holds an MBA from UC San Diego Rady School of Management and has spent over 15 years researching, writing, and advising on student loans, 529 plans, financial aid programs, and saving and investing for young professionals.

Robert has been featured in the The New York Times, The Wall Street Journal, The Washington Post, NBC News, and Forbes, where he has been a regular personal finance contributor for over a decade. His work combines both professional expertise and personal experience – he successfully navigated his own student loan repayment journey and has helped thousands of readers do the same.

He is committed to making the intersection of personal finance and education transparent and accessible. You can learn more about Robert on the About Page or on his personal site RobertFarrington.com.